Family and Legacy Fund Difference: Which Is Right for Your Wealth Plan?

The difference between a Family Fund & a Legacy Fund, & how combining both creates a balanced, intentional approach to wealth, estate, and retirement planning.

When we talk to our clients about retirement and estate planning, the question of legacy often comes up and they ask, “how much will I have leftover at the end and what can I do with it?”

This naturally leads us to talk about gifting money, and if they want to do it while they’re alive or wait to pass it on through their will.

Both approaches have their benefits, and it really comes down to what you can afford in the present and if you want to be around to see your loved ones enjoying your gift. No matter what you choose, understanding the difference between a family and legacy fund is important when you talk to your financial advisor.

In a nutshell, a Family Fund supports the people you care about today and a Legacy Fund supports the people you’ll care about in the future. Together, they create a balanced approach of living well now and leaving something meaningful behind as part of broader retirement and estate planning.

Below you’ll see a breakdown of the key differences to bring to your financial planning discussions, and a real-world example to help give context.

What Is a Family Fund?

This is a pool of money that supports your household’s needs during your lifetime. It’s flexible, easy to access, and designed for the next few years—not the next few decades. Many families begin this work by asking the 20 questions to ask before retirement and mapping short-term priorities.

It supports goals like helping your children with tuition, providing support to aging parents, or paying for unexpected expenses along the way.

Common tools used for Family Funds include:

- TFSAs (source of tax-free funds)

- RESPs (specifically designed for educational savings)

- Cash reserves and high-interest savings accounts

- Non-registered investment accounts

- Short- to medium-term investment portfolios

It is important to have liquidity and stability in whatever fund structure you choose because life happens—and your family often needs resources quickly.

What Is a Legacy Fund?

A Legacy Fund is different—this is where you plan for the generations to come and not just your lifetime needs. The goal is long-term wealth preservation and intergenerational impact. This is where estate planning for business owners and professional families becomes especially important.

Legacy Funds usually use more formal structures—like trusts or holding companies—and these usually involve rules about how and when money can be used. This is where estate planning becomes really important because there is often more wealth to pass on and existing business structures to consider.

Many Canadians build their Legacy Fund using a combination of corporate assets, permanent life insurance, estate transfers, or various planned giving options and charitable structures.

The goal is to grow and protect your wealth, so it serves more than a single generation.

Common tools used for Legacy Funds include:

- Trusts

- Holding companies

- Permanent life insurance

- Donor-advised funds or private foundations

- Endowments

- Will-based strategies and advanced directives

Because the time horizon is so long, these funds can take on a more growth-oriented investment strategy to help your money keep up with inflation and preserve its purchasing power.

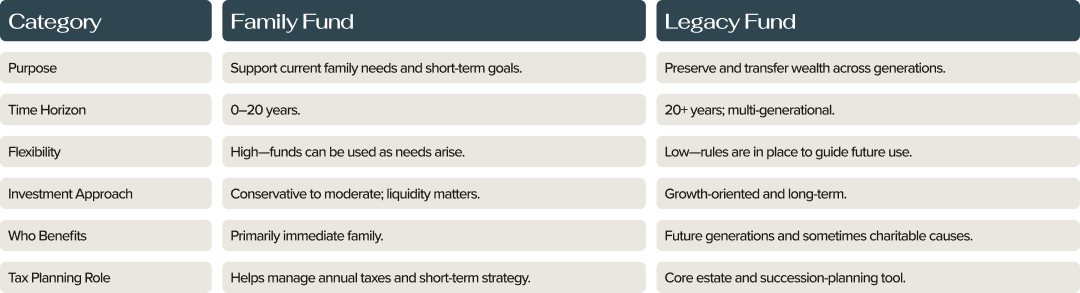

Side-by-Side Comparison: Family and Legacy Fund Difference

Here’s a quick comparison to highlight the differences:

Why This Matters

Many Canadians focus on retirement saving, but fewer take the next step and ask:

“What happens to my wealth when I’m gone?”

Resources like 101 things to do when you retire and 7 documents you need to fill out before you die often help start these conversations.

Building both a Family Fund and a Legacy Fund answers that question with intention and often includes professional legacy planning services to ensure nothing is left to chance.

A Real-World Example: How a Family Fund and Legacy Fund Work Together

Meet Sarah and David (names changed).

They’re both in their mid-50s, live in BC, and are approaching their peak earning years. Sarah owns a successful professional corporation, and David works in a senior management role. They have two teenage children and aging parents on both sides.

Their Family Fund (Today’s Priorities)

Sarah and David’s Family Fund is designed to support their life now and over the next 10–15 years.

It includes:

- RESPs for both children, on track to fund most post-secondary costs

- TFSAs used for medium-term goals and tax-free flexibility

- A high-interest savings reserve for emergencies and home repairs

- A non-registered investment account earmarked for helping the kids with a future down payment

This fund gives them confidence. If one child needs extra schooling, a parent needs temporary support, or an unexpected expense arises, they can act quickly—without disrupting long-term plans.

Their Legacy Fund (Long-Term Vision)

At the same time, Sarah and David want to ensure that their wealth doesn’t disappear within a generation. Their Legacy Fund focuses on what happens after their lifetime.

It includes:

- Retained earnings inside Sarah’s professional corporation

- A family trust named in their estate plan

- Permanent life insurance to fund taxes on death and provide liquidity

- A written legacy statement outlining how funds can be used for education, first homes, or entrepreneurship

The trust specifies that future distributions are limited to education costs, major life milestones, and a capped annual amount—helping protect beneficiaries from receiving too much, too soon.

How the Two Funds Work Together

- The Family Fund handles real-time needs with flexibility and access.

- The Legacy Fund provides structure, tax efficiency, and long-term protection.

- If the Family Fund is drawn down in a high-expense year, the Legacy Fund remains untouched.

- On death, the Legacy Fund absorbs estate taxes and continues supporting future generations without forced asset sales.

The Outcome

Sarah and David gain peace of mind knowing:

- Their children are supported today

- Their estate plan is intentional, not accidental

- Their wealth has purpose beyond their lifetime

So, the family and legacy fund difference? It’s the difference between supporting the people you love now with flexibility and intention, and protecting the people you’ll love later with structure, foresight, and lasting impact—together creating a wealth plan that serves both your life and your legacy.

At Relay Wealth, legacy is built into our name, and it is something we are passionate about. As a third-generation family business we understand estate planning for business owners and individuals. We know firsthand the benefits of generational wealth planning and are here if you need support in your planning.

Charlotte Starkey is a Wealth Advisor with CI Assante Wealth Management Ltd. The opinions expressed are those of the author and not necessarily those of CI Assante Wealth Management Ltd. Please contact her at (250) 475-6700 or visit www.relaywealthadvisors.com to discuss your particular circumstances prior to acting on the information above.

The case study mentioned in this presentation is provided for illustrative purposes only and does not represent an actual client or an actual client’s experience, but rather is meant to provide an example of our process and methodology. The results portrayed is not representative of all of our clients’ experiences.

CI Assante Wealth Management Ltd. is a Member of the Canadian Investor Protection Fund and the Canadian Investment Regulatory Organization.